Contribution Margin: What it is and How to Calculate it

For each type of service revenue, you can analyze service revenue minus variable costs relating to that type of service revenue to calculate the contribution margin for services in more detail. The overall contribution margin is computed using total sales and service revenue minus total variable costs. Typical variable costs include direct material costs, production labor costs, shipping supplies, and sales commissions. Fixed costs include periodic fixed expenses for facilities rent, equipment leases, insurance, utilities, general & administrative (G&A) expenses, research & development (R&D), and depreciation of equipment.

Fixed cost vs. variable cost

Contribution margin calculation is one of the important methods to evaluate, manage, and plan your company’s profitability. Further, the contribution margin formula provides results that help you in taking short-term decisions. As a business owner, you need to understand certain fundamental financial ratios to manage your business efficiently. These core financial ratios include accounts receivable turnover ratio, debts to assets ratio, gross margin ratio, etc. Now, divide the total contribution margin by the number of units sold. A contribution margin analysis can be done for an entire company, single departments, a product line, or even a single unit by following a simple formula.

Variable Costs

Using this metric, the company can interpret how one specific product or service affects the profit margin. The fixed cost like rent of the premises, salary, wages of laborers, etc will remain the same irrespective of changes in production. So it is necessary to understand the breakup of fixed and variable cost of any production process. You might wonder why a company would trade variable costs for fixed costs.

What is the Contribution Margin Ratio?

Furthermore, per unit variable costs remain constant for a given level of production. Variable costs are not typically reported on general purpose financial statements as a separate category. Thus, you will need to scan the income statement for variable costs and tally the list. Some companies do issue contribution margin income statements that split variable and fixed costs, but this isn’t common.

After all fixed costs have been covered, this provides an operating profit. An important point to be noted here is that fixed costs are not considered while evaluating the contribution margin per unit. As a result, there will be a negative contribution to the contribution margin per unit from the fixed costs component. Conceptually, the contribution margin ratio reveals essential information about a manager’s ability to control costs. Knowing how to calculate the contribution margin is an invaluable skill for managers, as using it allows for the easy computation of break-evens and target income sales.

- For example, if the cost of raw materials for your business suddenly becomes pricey, then your input price will vary, and this modified input price will count as a variable cost.

- Furthermore, sales revenue can be categorized into gross and net sales revenue.

- Therefore, it is not advised to continue selling your product if your contribution margin ratio is too low or negative.

- Thus, the level of production along with the contribution margin are essential factors in developing your business.

- Conceptually, the contribution margin ratio reveals essential information about a manager’s ability to control costs.

- By analyzing the unit contribution margin of different products or units, companies can identify their most profitable offerings and allocate resources accordingly.

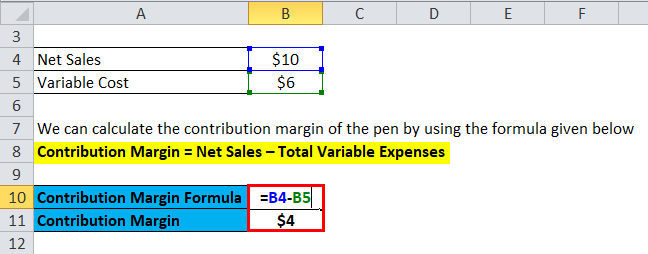

Variable costs, on the other hand, increase with production levels. In the same example, CMR per unit is $100-$40/$100, which is equal to 0.60 or 60%. So, 60% of your revenue is available to cover your fixed costs and contribute to profit. Decisions can be taken regarding new product launch or to discontinue the production and sale of goods that are no longer profitable or has lost its importance in the market. The contribution margin is the amount of revenue in excess of variable costs. One way to express it is on a per-unit basis, such as standard price (SP) per unit less variable cost per unit.

Before making any changes to your pricing or production processes, weigh the potential costs and benefits. The contribution margin is important because it gives you a clear, quick picture of how much “bang for your buck” you’re getting on each sale. It offers insight into how your company’s products and sales fit into the bigger picture of your business. If the contribution margin for a particular product is low or negative, it’s a sign that the product isn’t helping your company make a profit and should be sold at a different price point or not at all. It’s also a helpful metric to track how sales affect profits over time. Let’s say we have a company that produces 100,000 units of a product, sells them at $12 per unit, and has a variable costs of $8 per unit.

Therefore, we will try to understand what is contribution margin, the contribution margin ratio, and how to find contribution margin. This metric is typically used to calculate the break even point of a production process and set the pricing of a product. They also use this to forecast the profits of the budgeted production numbers after the employee evaluation form templates prices have been set. If the company realizes a level of activity of more than 3,000 units, a profit will result; if less, a loss will be incurred. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing.

Write a Comment